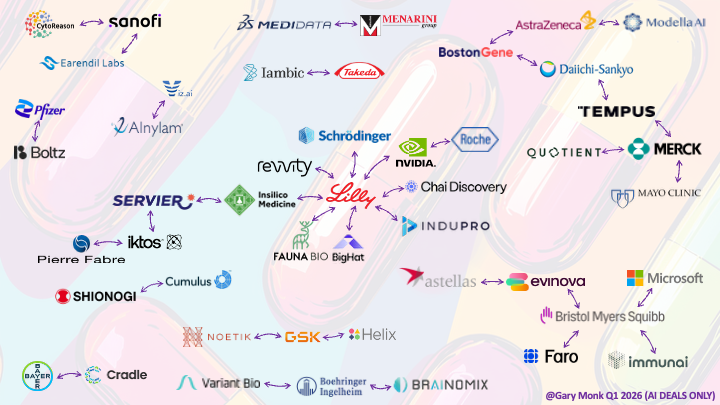

Q1 2026 was a turning point for artificial intelligence in pharma. But it was not about the number of deals, although that number was significant. Doubling to thirty-six major AI partnerships in Q1 2026 versus eighteen in Q1 2025.

It is what sits behind those deals that really matters.

We are seeing AI activity that spans multiple pharma domains

simultaneously: drug discovery, diagnostics, clinical development, and now

embedding itself into the deeper plumbing of manufacturing and commercial

functions. As well as breadth, we are seeing depth. AI integrating itself

profoundly into the pharma operating model rather than sitting alongside it as

an innovation experiment.

The deals announced between January and March were not pilots. They were

architectural decisions. Multi-year terms. Billion-dollar values. Third and

fourth extensions on relationships that were already mature. And in at least

one case, an acquisition to a recent partnership. Taken together they tell a

story about an industry that has stopped asking whether AI works and started

asking how to build around it permanently.

The Lilly Blueprint

In Q1 no company was a better exemplar than Eli Lilly. Eight

significant AI partnerships in a single quarter is extraordinary by any

measure, but the structure of those deals is more revealing than the volume.

Lilly literally bet all its chips on

AI-enabled drug discovery this quarter. The first company to deploy NVIDIA's

DGX B300 AI supercomputer, co-investing over $1 billion in a co-innovation lab

alongside it. Capital expenditure at this scale does not get unwound at the

next budget review.

The Insilico Medicine collaboration, worth up to $2.75 billion, is

not a discovery bet on a single programme. It is a platform commitment across

multiple targets and therapeutic areas with milestone-driven payments tied to

pipeline progress.

Then there is TuneLab. Lilly's federated AI model network, trained

on over a billion dollars of proprietary data, expanded across Schrödinger,

Revvity and BigHat in Q1. The logic is self-reinforcing: more

partners generate more diverse training data, which improves the models, which

attract more partners. Lilly is not just building internal capability.

It is positioning itself as the connective tissue of an industry-wide AI

discovery ecosystem, opening the doors to collaborators who can access Lilly

data across a federated interface.

Alongside this, partnerships with Chai Discovery for biologics, InduPro

for oncology membrane interactomics, and Fauna Bio for obesity target

discovery, inspired by how hibernating animals regulate weight and metabolism,

round out a portfolio that jointly spans biology, chemistry, compute and

platform infrastructure.

Bristol Myers Squibb: Four Deals, Three Domains, One

Quarter

Where Lilly went deep on discovery infrastructure, BMS went

broad. Four distinct AI partnerships spanning drug discovery, diagnostics and

clinical development in a single quarter is a portfolio strategy, not a series

of one-off decisions.

Immunai brought AI-driven immune analysis

into BMS clinical programmes, generating insights that inform patient

stratification and feed back into discovery decisions. Microsoft brought

AI radiology into lung cancer detection, embedding FDA-cleared algorithms into

clinical workflows already operating across most US hospitals. Evinova

brought agentic AI into trial design, enabling BMS to scenario-plan and

optimise protocols before studies begin, shifting from running more trials to

running better ones. And Faro brought AI upstream into protocol drafting

and benchmarking, turning trial design into structured, optimisable

infrastructure rather than a manual drafting exercise.

Each deal targets a different bottleneck. Together they suggest a

deliberate attempt to embed AI across the entire development cycle rather than

concentrate it in one area.

The Structure Signal

The rest of the map tells the same story from different angles.

Daiichi Sankyo ran two AI deals

with a specific strategic logic: as antibody-drug conjugates become more

competitive, patient selection becomes the differentiator. BostonGene

applied AI-powered digital twin models to refine which patients are most likely

to respond to Daiichi's ADCs. Tempus brought in its PRISM2

foundation model to strengthen biomarker discovery and stratification across

the same pipeline. Two deals, two tools, one objective: getting the right

patients into the right trials.

Merck ran three deals: a genomics platform

with Quotient Therapeutics for IBD target identification, a virtual cell

collaboration with Mayo Clinic running AI models inside Mayo's secure

environment on multimodal clinical data, and a Tempus partnership for

precision oncology. GSK partnered with Noetik on virtual cell

modelling for tumour biology and with Helix for population-scale

genomics. Servier signed two major generative AI deals in a single week,

Insilico and Iktos, with Pierre Fabre following Iktos

into a separate collaboration shortly after.

Bayer and Cradle committed to a

three-year protein engineering collaboration. Boehringer Ingelheim

partnered with Variant Bio on kidney disease target discovery and with Brainomix

on AI imaging as a co-primary endpoint in a Phase III pulmonary fibrosis trial.

Using AI output as regulatory evidence is a significant escalation from using

AI as an internal decision support tool, and a signal of how far that

particular partnership has matured. Sanofi extended its CytoReason

relationship for the third time and partnered with Earendil Labs on an

autoimmune bispecific programme in a deal that could reach $2.5 billion.

And then there is AstraZeneca and Modella AI. AZ's shotgun

wedding with its medical AI imaging partner, acquired outright just months

after initiating the partnership, is perhaps the best poster child of an

industry that wants to build AI capabilities into its operating system rather

than access them at arm's length. Partnership was no longer enough.

What This Quarter Actually Means

The pilot phase of pharma AI had a recognisable signature: short

engagements, narrow scope, single programmes, cautious language around proof of

concept. Q1 2026 had almost none of that signature.

What it had instead was duration, scale, specificity and repetition.

Companies returning to partners they already trusted and committing more.

Companies building compute infrastructure they will depreciate over years.

Companies embedding AI into clinical workflows as standard operating procedure.

Companies acquiring rather than partnering when the strategic fit was clear

enough.

The industry did not suddenly discover that AI works in Q1 2026. What

happened is that enough internal evidence accumulated, across enough

programmes, enough organisations, enough functions, that the case for permanent

infrastructure finally outweighed the case for continued experimentation.

Thirty-six deals. Double the prior year. But that number is still the

least interesting thing about this quarter.